1 in 3 Cyber Insurance Claims Are Being Denied & Here’s Why

An alarming 43% of all cyberattacks target small and mid-sized businesses, underscoring their critical vulnerability in the digital landscape. The repercussions of such attacks are severe, with roughly 60% of breached small and mid-sized businesses closing their doors permanently within six months. Compounding this risk, a significant number of Canadian businesses are discovering that their cyber insurance, intended as a financial safety net, isn’t always reliable. Reports indicate that approximately one in three cyber insurance claims are being denied, leaving businesses exposed to devastating financial losses.

Across Canada, businesses are increasingly reliant on cyber insurance to mitigate the financial impact of breaches. Yet, the high rate of denied claims reveals a critical disconnect between a business’s perceived security posture and the stringent requirements of insurance providers. Understanding the core reasons behind these denials is crucial for any organization aiming to protect itself effectively.

The Evolving Landscape of Cyber Insurance

Cyber insurance has emerged as an essential component of risk management, offering financial protection against a range of incidents from data breaches to ransomware attacks. However, as the frequency and sophistication of cyber threats have escalated, insurers have significantly tightened their underwriting standards and claim processes. Policies that once seemed straightforward now come with intricate clauses and strict preconditions that many businesses fail to meet. This shift reflects a market adjusting to substantial losses, making it imperative for policyholders to demonstrate robust and verifiable security measures.

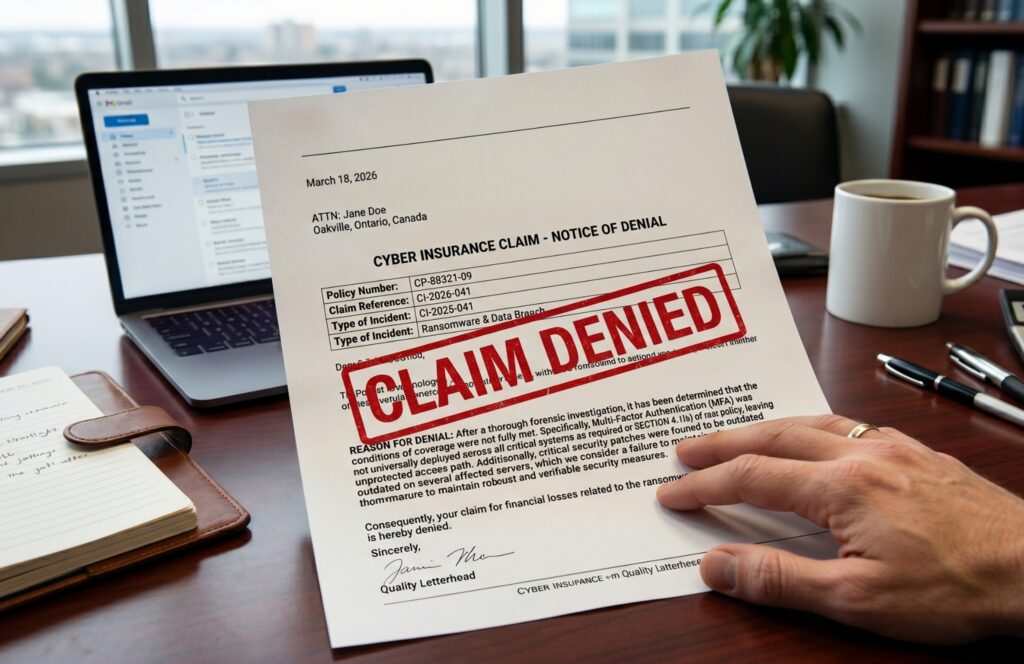

Inadequate Security Controls: A Primary Culprit

One of the most frequent reasons for claim denials stems from a business’s inadequate security controls. Insurers expect policyholders to have fundamental cybersecurity measures in place as a condition of coverage. When a breach occurs, a forensic investigation often reveals gaps in these controls, leading to a denial.

Common deficiencies include:

- Missing or Incomplete Multi-Factor Authentication (MFA): Many claims are denied because Multi-Factor Authentication was not fully deployed across all critical systems, remote access points, and administrative accounts. Even a single unprotected path can be enough for attackers to gain access and for an insurer to deny coverage.

- Outdated or Unpatched Systems: Failure to apply security patches and updates promptly leaves known vulnerabilities exposed. Insurers may argue that a breach exploiting such a vulnerability was preventable, leading to a denial.

- Lack of Endpoint Detection and Response (EDR): Without robust EDR solutions, businesses may lack the ability to detect and respond to advanced threats on their devices, which is a key requirement for many modern policies.

- Insufficient Data Backup and Recovery: Many policies mandate regular, tested data backups, often requiring offsite or air-gapped copies. If data cannot be recovered, or if the backup process was flawed, claims can be denied.

- Weak Access Controls and Network Security: Poorly managed user access, weak passwords, or a lack of proper network segmentation can all be grounds for denial, as they represent fundamental security failings.

Unproven Compliance and Documentation Gaps

Simply having security controls in place is often not enough; businesses must also be able to prove their implementation and ongoing effectiveness. Insurers are increasingly scrutinizing whether policyholders misrepresented their security posture during the application process, even unintentionally.

Consider a scenario where a business owner affirms they have a particular security measure, only for an incident to reveal that the control was not fully operational or adequately maintained. Without clear documentation and an auditable history of compliance, insurers may reject the claim. This is where continuous compliance management becomes invaluable.

TruPoint Technology Services Ltd. understands this critical need for verifiable compliance. TruCompliance tracks the details of our Client’s Cyber Insurance policy, including critical wordings for requirements, controls, and definitions. This allows our Clients to confidently manage technology risks against their Insurance. This proactive approach ensures that Canadian small and mid-sized businesses can demonstrate a consistent and robust security posture, providing the necessary evidence should a claim arise.

Failure to Meet Policy Stipulations and Exclusions

Cyber insurance policies are complex legal documents, often containing specific stipulations and exclusions that businesses overlook or misunderstand. These can be buried in the “fine print” and become significant hurdles during a claim investigation.

Common policy pitfalls include:

- Exclusions for Specific Attack Types: Some policies may have exclusions for certain types of cyberattacks, such as those originating from third-party vendors or specific nation-state actors, unless explicitly endorsed.

- Late Notification of an Incident: Policies almost universally require prompt notification of a cyber incident. Delays in reporting, even by a few days, can be used by insurers to deny a claim, arguing that the delay hindered their ability to investigate or mitigate damages.

- Lack of an Incident Response Plan: Many policies require a documented and tested incident response plan. If a business cannot demonstrate that it had a clear strategy for detecting, responding to, and recovering from an attack, the claim may be jeopardized.

- Misrepresentation on the Application: Providing inaccurate or incomplete answers on the insurance questionnaire, even without malicious intent, can be grounds for a denial. Insurers will conduct thorough investigations to verify the information provided.

From Annual Audit to Always-On Compliance: The New Standard

The landscape of cyber threats and insurance requirements demands a shift from a reactive, checkbox mentality to a proactive, continuous compliance posture. Relying solely on annual audits or a one-time assessment is no longer sufficient. Security must be an ongoing, managed capability, deeply integrated into daily operations.

For security-minded businesses, particularly those in regulated sectors such as financial services, this means:

- Continuous Monitoring and Threat Detection: Implementing advanced monitoring tools like Extended Detection and Response (XDR) and Security Information and Event Management (SIEM) provides real-time visibility into an organization’s network and endpoints, enabling rapid detection of threats.

- Managed Information Security Management Systems (ISMS): A structured ISMS, often aligned with standards like ISO 27001 or SOC 2, ensures that security policies and procedures are consistently managed, reviewed, and improved. This provides a clear framework for demonstrating ongoing compliance.

- Virtual Chief Information Security Officer (Virtual CISO) Services: Many small and mid-sized businesses lack the internal resources for a dedicated Chief Information Security Officer. A Virtual CISO offers expert guidance, helping businesses develop and maintain their security strategy, manage risk, and navigate complex compliance requirements.

- Regular Penetration Testing and Vulnerability Assessments: Proactively identifying weaknesses through regular testing helps strengthen defenses before attackers can exploit them.

- Ongoing Cybersecurity Training: Employees are often the first line of defense. Regular and comprehensive training helps them recognize and respond to threats like phishing, reducing the risk of human error.

Building an Evidence Trail That Survives an Insurance Claim or Regulatory Review

To confidently navigate the complexities of cyber insurance and regulatory scrutiny, businesses must focus on building a robust evidence trail. This means not just implementing security controls, but continuously documenting and verifying their effectiveness.

Key actions include:

- Detailed Logging and Auditing: Maintain comprehensive logs of all security events, access attempts, and system changes. These logs are crucial for forensic investigations and for proving that controls were operational at the time of an incident.

- Policy and Procedure Documentation: Ensure all cybersecurity policies, incident response plans, and data handling procedures are thoroughly documented, regularly updated, and clearly communicated to all employees.

- Regular Assessments and Reporting: Conduct periodic risk assessments, vulnerability scans, and penetration tests, and retain all reports. These demonstrate due diligence and an proactive approach to security.

- Training Records: Keep meticulous records of all employee cybersecurity training, including attendance, topics covered, and assessment results.

By prioritizing an always-on approach to security and compliance, businesses can not only strengthen their defenses against cyberattacks but also ensure that their cyber insurance provides the protection they expect, when they need it most.

Key Takeaways and Next Steps

The rising rate of cyber insurance claim denials serves as a stark warning: robust cybersecurity is no longer merely a technical consideration but a business-critical imperative. Canadian small and mid-sized businesses must move beyond basic security measures and embrace a continuous, verifiable approach to compliance. This involves implementing strong controls, maintaining meticulous documentation, understanding policy nuances, and adopting a proactive security culture.

TruPoint Technology Services Ltd. is a 100% Canadian owned and operated managed services and cloud service provider, purpose-built to deliver full-stack Zero Trust IT to security-minded businesses. Our flagship service, TruWorkspace Zero Trust™, wraps every device, user, and application in a modern security architecture. Furthermore, TruCompliance™ is our proprietary compliance management service, combining a Virtual CISO, managed ISMS software, SOC/XDR/SIEM monitoring, penetration testing, and cybersecurity training to help customers achieve and maintain compliance continuously. For businesses seeking to strengthen their security posture and ensure their cyber insurance truly protects them, exploring a comprehensive, managed security and compliance solution is the essential next step.

To learn how TruPoint can help your business navigate the complex world of cybersecurity and compliance with confidence, contact us here.

Sources

- Current time information in Canada.

- Top 6 Reasons for Cyber Insurance Claim Denials | The AME Group.

- Top 5 Reasons Why Businesses Are Denied Cybersecurity Insurance Coverage.

- Cybersecurity Insurance Requirements in Canada: A Comprehensive Guide.

- Why 4 in 10 Cyber Insurance Claims Are Denied.

- Understanding why Cyber Insurance Claims fail – Somniac Security.

- 82% of Cyber Insurance Denied Claims Had One Thing in Common.

- Denied Cyber Insurance Claim? Your Legal Options.

- Canadian SMBs Face Rising Cyberattacks in 2025 – Employment Hero (CA).

- Cybercrime: Is your small business protected? – CFIB.

- Survey of cybersecurity and Canadian SMEs – BDC.

- How To Meet Cyber Insurance Requirements In 2024 | Microserve Canada.

- 10 Cybersecurity Controls That Could Make or Break Your Cyber Insurance Policy.

- How to Meet Cyber Insurance Requirements (and Avoid Denied Claims) – Zero Networks.

- Mistakes that Void Cyber Insurance | 3rd Element Consulting.

- 5 Cyber Insurance Requirements Insurers Verify Before Approving Claims – BNMC.

- The Daily — Impact of cybercrime on Canadian businesses, 2023.

- Cyber Insurance: How Canadian Businesses Qualify – Revolution Networks.

- Why Cyber Insurance Claims Get Rejected – Prelude.

- Data Breaches in Canada: Lessons Learned from Recent Cyber Attacks.

- Cyber Insurance Checklist 2026: 14 Controls SMBs Need – Fusion Computing.

- Cyber readiness: A new requirement for cyber insurance? – Financial Post.

- Navigating the Cyber Insurance Claims Process.

- 9 Important Cybersecurity Insurance Requirements (and How to Meet Them) – AllCovered.

- Coalition’s 2026 Cyber Claims Report Finds Initial Ransom Demands Surged 47% — But Most Businesses Refuse to Pay.

- The-most-common-cyber-claims-in-Canada.

- What is driving the cost of cyber claims in Canada? | HSB Canada – Munich Re.

- Canada’s cyber insurance market finds its footing, despite an evolving threat landscape.

- SMEs aren’t the problem in cyber uptake – the market is, says CFC cyber chief.

Content Integrity

This article was generated with the assistance of AI and edited by a human team member.